Advanced warning – minor spoiler alerts, but don’t worry we don’t give away any of the juicy stuff. Join us as we explore the tropes of Squid Game from the perspective of fintech expertise. For those fighting the curve and have yet to watch Squid Game, it is in essence about 456 Koreans who are engulfed by debt which they are unable to repay because they’ve been exploited by hidden fees and endless debt. Being invited to a mysterious competition, with little to no details, they attend and play games from their childhood with the opportunity to win a huge sum of money. The catch is that if you fail one of the games, you meet your fatal end and are shot. Brutal, right? Squid Game offers us similar thrills to the Saw franchise. For those of us within financial and fintech services, it poses a clear commentary on financial inequality and a general lack of accessibility to traditional financial services.

Starting at the beginning, the first episode shows us a scene of a ‘salesperson’ who offers one of our heavily indebted characters, Seong Gi-hun, a game of ddakji. The betting game was simple and if Seong Gi-hun won, he could potentially earn large sums of money from the mysterious salesperson. Seong questions whether it’s a scam – something which resonated with us highly. In numerous places, particularly that of the Asia-Pacific countries, financial accessibility is fragmented and scarce. Thus, the prospect of opening an account to manage their finances isn’t on the cards (get it? Cards… banking… *laughs in fintech*).

The cost? Merchants controlling their business’ finances with a bank account are hindered by transfer fees, account fees, etc. which impact their margins. Traditional banking methods adopt innovations at a slower rate than desired; impacting the business transformation process for merchants, which would facilitate international growth and accepting payments via multiple methods. During Squid Game’sgame of ddakji, this is represented as Seong takes a hit each time he loses a round of the game, facing numerous hits before he reached a profit – literally! (Did you see how red his face got after each slap?). Arguably this comments on the ‘hits’ a merchant endures on their journey with traditional banking; in which they are burdened by lengthy time constraints and costs which eat into their profit margin.

In such a fluid time of digitalisation, filled with alternative payment methods and solutions, traditional banks now appear to be restricted in movement and heavily regulated with processes, such as Basel III. Consequently, banks deflect costs onto merchants with opening fees, manual checks, minimum account fees and strenuously low interest rates.

“I know you’re doing your job, but I don’t have time to sit here” – Seong Gi-hun

There is a moment which really made us think of start-ups and budding businesses who seek the support of banks with a secure account to manage their payments. In a digitally booming world, and the humungous markets within the APAC regions, merchants are grappling at the chance to enter new landscapes and advance their businesses. Seong’s quote above summarises the speed of traditional banking in comparison to our digitally evolving landscape. Payment methods emerge regularly to compete with rising urbanisation and smartphones. Whilst traditional banks function as a regimented steppingstone into the financial world, fintech plugs the entire gap by providing holistic solutions at a quicker speed. Traditional banking methods have engrained banking processes, gradually cultivated over decades, in turn making them slower to adapt to change. Seong’s impatience isn’t uncommon in the commercial world. As fintech responds to the growing demand of our tech-savvy world, merchants are now able to bypass traditional avenues for 24/7 and fast access to payment solutions such as digital banking, open banking, neobanks and much more.

How will fintech bring accessibility in the Asia Pacific region?

Asia’s financial fragmentation calls for a wide scope of innovative solutions, to provide equal opportunities and maturation. Over 1 billion people in the APAC region still do not have access to formalised financial services. Moreover, nearly 75% of the population in South-East Asia, is either underbanked or completely unbanked. Numerous stipulations for businesses and consumers have limited access to traditional banking opportunities; and thus driven the use of ecommerce platforms and alternative payment methods. During Squid Game’s episode of chaos and crossed loyalties, the leader interjects the unfair treatment between players: “you ruined the most important aspect of this place… Equality. Everyone is equal while they play this game. Here, every player gets to play a fair game under the same conditions. These people suffered from inequality and discrimination out in the world, and we’re giving them one last chance to fight fair and win.” Righteousness aside, this is pretty heavy stuff but neatly summarises the perspective of fintech innovators, including Unlimit.

South Korea’s new lending curb brought into place in summer 2021 are only a single example of how financial accessibility remains unequal. A merchant with a strong credit record and financial capabilities of paying higher interest rates is still likely to face rejection when applying for a loan or bank account. With banks cutting loans, merchants of start-ups and expanding businesses consequently turn to higher cost lenders to evade restrictions.

Fintech solutions bring promising entry pathways into a secure, advanced financial world which is accessible to all. ‘Buy now, pay later’ (BNPL) is a key driver for commercial movement. Atome and Hollah being two of the most popular leaders of the industry, with easy repayment options across several months and as little as 0% interest.

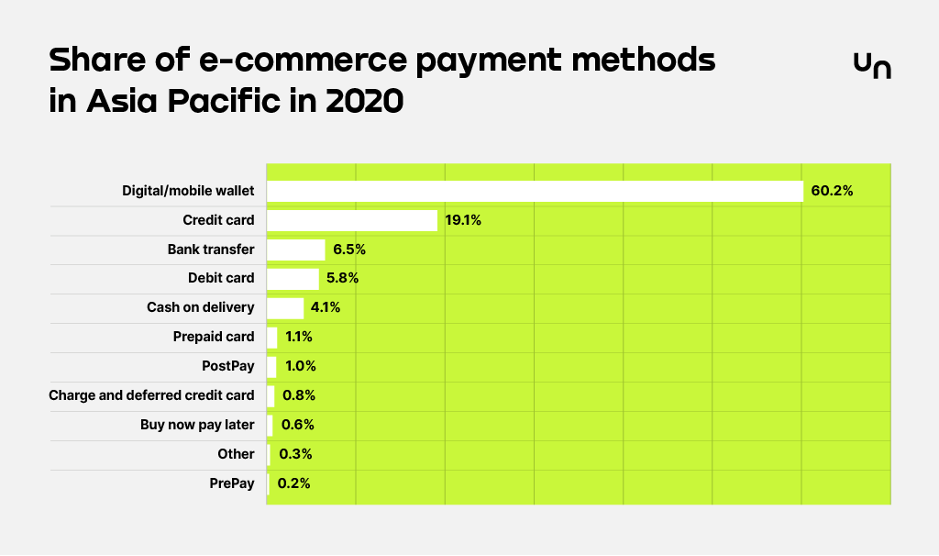

For areas of Asia which are economically driven by cash on delivery and offline payments, methods such as digital wallets and the use of EKYC are valuable. Rapid access and simplified account set up in real-time is now able to take place in less than an hour. Solutions, including BNPL and EKYC, provide transparency, security, and easy-to-use methods with far fewer joining criteria. Advances in innovation support merchants who look to fintech to help them scale their business across numerous markets and simplify the launch to market. Platforms who are accelerating technologies, with targeted audiences are playing a significant role in a merchant’s progression and expansion. Development of a more equalised access to market has meant that Asia Pacific’s e-commerce sales are expected to nearly double by 2025, reaching heights of 2 trillion USD.

The future of financial services within the APAC region is bright and competitive. We see traditional financial institutions moving towards digitalisation, be it at their own pace. Technologies within fintech are now shaping the economy, eroding the limitations of traditional banking methods. Such fluidity will only create better opportunities for merchants to expand their businesses and reach global heights. Additionally, with such a large population and scope for development, international businesses are venturing to Asia to launch business ideas.